The focus of our research methodology is to provide a reasonable basis to identify the best superannuation solution for a client. As such our focus is on the performance, price, features, benefits and sustainability relative to customer requirements and risk tolerance levels. Product recommendations are made after reviewing client requirements and optimising outcomes over time. We have performance and pricing research on over 5000 superannuation and pension funds that exist in Australia and we use this to rate and score super funds for you. Each super fund is rated and given an overall score based on the following weightings.

Components of the overall score

An overall score for a super fund is based on two components, firstly the underlying investments and fees which are unique to the selection, or default allocation of investments chosen by an individual and secondly the features, benefits and size, that are applicable to the product a person is in. The score reflects an assessment under these 4 broad categories:

- Performance we consider returns annualised over one, three, five and ten years relative to peers in the same risk category. The returns are net of direct and indirect investment fees of the funds, but before the deduction of administration fees and any adviser fees.

- Price of investments, the fund administrative costs and ‘other fees.

- Features and benefits of a fund, which may include availability of investments, access to pensions, tax benefits, availability of specific investment types, like term deposits and more.

- Size of the fund as a measure of gross funds under management.

Super Fund performance versus risk

Superannuation performance must always be measured relative to risk. For this reason, each superannuation fund review begins with identification of the asset allocation of funds underlying investments. Our performance versus risk and benchmark analysis is designed to avoid unfair, biased perspectives regarding a super fund. For this reason alone, we ask clients to provide information related to existing superannuation funds.

Price versus features

Each purchaser of a superannuation product has a unique set of personal circumstances. Some product features may be more or less valuable to them than to other purchasers. The attractiveness of each feature will also depend on its price. We therefore take into account both features and price (as well as the financial strength of the super fund) in determining overall scores allocated to super funds.

For this reason, a product with very strong features may still not be rated highly if the price for those features is too high. Similarly, a product with fewer features than its competitors may still rate highly if its price is lower.

Research houses have been criticised for encouraging the proliferation of features that, some say, are of limited real value to customers. We believe our scoring methodology does not encourage such product developments because:

- A weight is applied to each feature and sub-feature which reflects its value to customers – features of low perceived value receive little or no weight.

- Where the super fund increases prices to pay for additional features, the price score for that product will reduce the overall product score.

The weight given to each feature and sub-feature reflects the frequency with which customers are likely to use that feature. The weight for features is also supported by data supplied by our investment research provider, Morningstar. When Retirement Services Australia receives updated data, the weights for each feature and sub-feature change as part of the ongoing review process.

Basis for scoring a super fund

The scoring methodology reflects information contained in research provided by our research providers and the following documents provided by superannuation funds:

- Product Disclosure Statements (PDS) and any Supplementary PDSs

- Policy documents (where available)

- Asset allocation reports

- Performance reports

- Commission guides

- Member statements and

- Price and rate tables.

We use comparative analysis data provided by APRA where possible to cross check the accuracy of the information provided.

Where certain product information is not disclosed in the documents above, we are sometimes required to accept other supplementary documentation, often from fund websites as evidence. However, whilst we reserve the right in exceptional circumstances to recognise such documents in the scoring process, our practice is not to do so on the grounds that Superannuation funds manage this content and web site information may be enhanced to include or exclude information at the discretion of product providers.

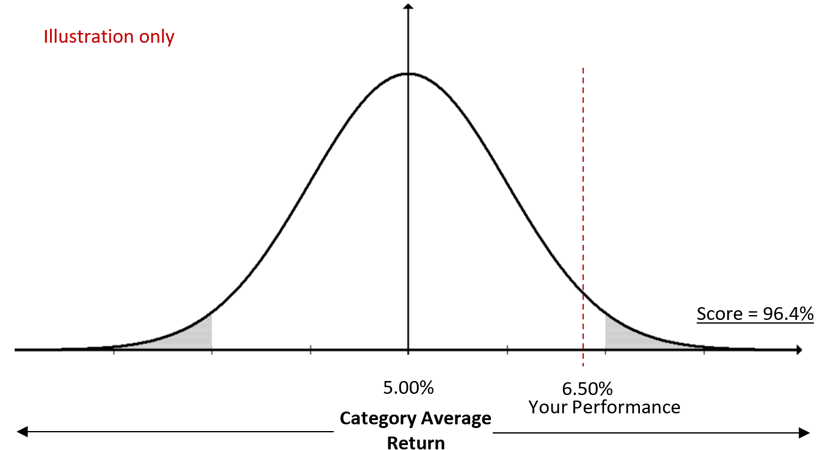

Performance score

Australians can access over 5,000 different investment options through hundreds of different superannuation funds. RSA monitor the investment asset allocation, historical performance and price of nearly 5000 investments. Our technology allows us to group investments by categories and provide a fair, quantifiable comparative analysis of customer investments. RSA monitor ASX listed securities and ETFs that are increasingly common components of investor super portfolios.

The primary factor used in formulating a score for the performance of an investment is historical annualised performance. This is compared to the average performance of all same category superannuation funds. Same category, defines a universe of superannuation funds with similar risk profiles and strategic asset allocation. For further information on the methodology applied to compute category average performance, please contact RSA.

Performance analysis overview

The process used to analyse performance is as follows:

- Identification of the risk profile and asset allocation of a customer’s existing super fund.

- Identify the category of the customer fund to determine the universe of similar funds for comparison.

- Compare the customer’s super fund performance relative to peers in the same risk profile or category.

For a detailed discussion regarding the quantitative computation of the performance score, please contact RSA .

For a detailed discussion regarding the quantitative computation of the performance score, please contact RSA .

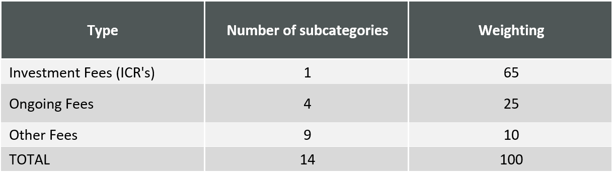

Price score

Super funds are required to adhere to ASIC’s guideline regarding cost disclosure detailed in Regulatory Guide 97. Price of superannuation products is sorted by type. Three types of fees contribute to the overall cost a customer may incur. Investment fees represent the cost of asset management services. Ongoing fees represent administrative and compliance fees that are charged annually and ‘other fees’ represent costs that may apply to a customer depending on their personal circumstance or approach to investing. A weighting is applied to each fee type based on the continuity of the cost and the likelihood of this cost being incurred. The price types and weightings are measured as follows:

We then calculate the price score by applying the same concept as the Return Score. This provides a particular score for the fees of your existing investment, relative to the average fees in the industry.

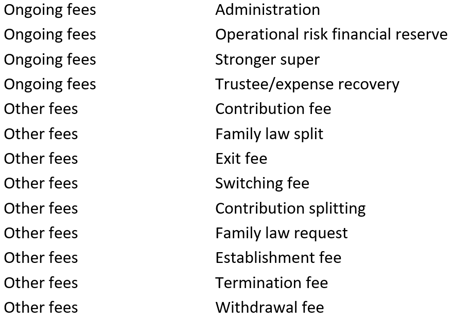

Pricing subcategories

Ongoing fees and other fees have a range of sub categories that we monitor to provide comparative analysis. They are as follows:

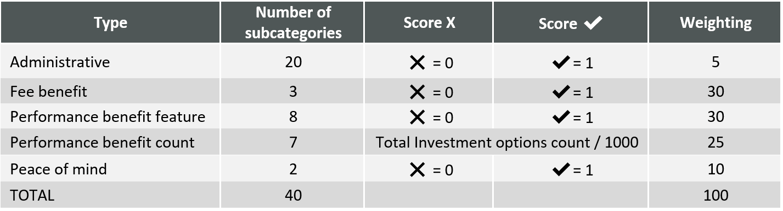

Features and investment selection score

Key features under each product and the strengths and weaknesses of those key features compared with other similar products in the market may be described in text, by existence or by count. Quantifiable features measured in terms of existence, either do or don’t exist within a product. Quantifiable features that are measurable by count, for example the number of investment options a customer can choose from are assessed numerically.

Measurement of product features in a quantifiable way, enables customers to consider a particular key feature and compare the strengths and weaknesses of each product in the market, for that particular feature.

Features are classed by type and have a relevance weighting applied based on our understanding of the relevance of the features to customers. The feature and score weightings are measured as follows:

Size score

The commercial strength of a product is based on the size of a products funds under management. Generally speaking, funds with greater funds under management are provided a higher rating than small funds. Larger funds are likely to be more sustainable, priced more competitively and have better systems to administer and manage superannuation on behalf of customers.